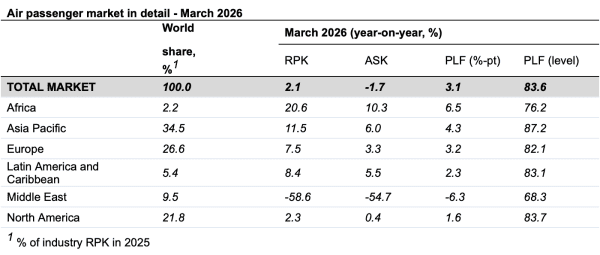

SINGAPORE, 6 May 2026: Travel demand, measured in revenue passenger kilometres (RPK), gained 2.1% in March 2026 compared with March 2025, according to the International Air Transport Association’s latest data.

IATA reported that capacity, measured in available seat kilometres (ASK), decreased 1.7% year-on-year. The load factor was 83.6% (+3.1 ppt compared to March 2025).

International demand fell 0.6% compared to March 2025. Capacity was down -6.2% year-on-year, and the load factor was 84.1% (+4.7 ppt compared to March 2025).

The overall decline in international traffic was driven by a -60.8% drop in the Middle East.

Meanwhile, domestic demand increased 6.5% compared to March 2025. Capacity increased 5.6% year-on-year. The load factor was 83.0% (+0.7 ppt compared to March 2025).

“Demand for air travel continued to grow in March despite disruptions in the Middle East. The nearly 61% decline in international traffic by carriers in the Middle East did, however, restrain global growth to 2.1%. Outside of the Middle East, demand grew by 8%,” said IATA’s Director General Willie Walsh.

“Everybody’s watching what’s happening with jet fuel—both supply and pricing. On the supply side, over the next few months, we could see shortages in parts of the world that rely heavily on Gulf supplies, especially in Asia and Europe. And the extraordinarily high cost of jet fuel is increasingly being reflected in ticket prices. While this has not impacted March traffic or forward bookings to date, it remains to be seen at what point high prices could start to shift passenger behaviour. So far, the summer is shaping up to be a normally busy time for travel. That’s positive news, but airline resilience is being tested and stabilising the supply and price of fuel is crucial. In the meantime, it’s important for regulators to be prepared to grant airlines some flexibility on slots, considering the extraordinary circumstances of airspace capacity restrictions and potential fuel rationing,” said Walsh.

Regional Breakdown – International Passenger Markets

International RPK fell -0.6%, the first decline since March 2021. This fall was due to a major decrease in traffic in the Middle East. In contrast, other international markets grew by 9%, and the passenger load factor rose in all regions except the Middle East.

Asia-Pacific airlines achieved an 11.5% year-on-year increase in demand. Capacity increased 1.5% year-on-year, and the load factor was 91.2% (+8.1 ppt compared to March 2025). Traffic in the region was boosted by the tail end of the Lunar New Year travel period, as well as by international routes (except those to the Middle East), which saw double-digit expansion.

European carriers saw a 7.7% year-on-year increase in demand. Capacity increased 3.2% year-on-year, and the load factor was 81.4% (+3.4 ppt compared to March 2025). Traffic between Europe and Asia surged 29.3% as direct services replaced traffic transiting through the Middle East.

North American carriers saw a 3.7% year-on-year increase in demand. Capacity increased 0.9% year-on-year, and the load factor was 85.5% (+2.3 ppt compared to March 2025). Transatlantic travel grew 3.3%, and the growth rate between Asia and North America more than doubled compared to February.

Middle Eastern carriers saw a 60.8% year-on-year decrease in demand. Capacity decreased 56.9% year-on-year, and the load factor was 67.8% (-6.6 ppt compared to March 2025). These figures are a direct result of the US-Israel-Iran war, which closed much of the airspace in the region.

Latin American airlines achieved a 12.1% year-on-year increase in demand. Capacity climbed 8.4% year-on-year. The load factor was 83.8% (+2.7 ppt compared to March 2025).

African airlines saw a 19.2% year-on-year increase in demand. Capacity was up 4.2% year-on-year. The load factor was 77.7% (+9.8 ppt compared to March 2025).

(Source: IATA)