BANGKOK, 25 March 2026: The current crisis in the Gulf did not emerge in isolation. It is the result of years of rising tension, shifting alliances and a gradual erosion of the diplomatic norms that once helped contain regional rivalries.

Decisions are also being taken faster. Responses are more immediate. And the space for quiet diplomacy has narrowed. What once unfolded over months is now compressed into days.

At the centre of the crisis lies a familiar axis: Iran, Israel and the US. Yet the dynamics have changed. This is no longer a contained confrontation. It is a conflict with global reach.

The early phase was marked by rapid escalation. Targeted strikes, counter-strikes and a surge in military readiness signalled intent on all sides. Each move carried a dual purpose: tactical gain and strategic messaging.

For Israel, the objective was clear. Act decisively and draw the US deeper into the confrontation. For Washington, the calculation has been more complex. Support an ally, project strength, but avoid a wider war that could spiral beyond control.

This tension defines the conflict

Public messaging suggests restraint. Military movements suggest preparation. The result is a strategic ambiguity that keeps all actors on edge.

Iran, meanwhile, is playing a longer game. Its response has been calibrated rather than impulsive. By avoiding immediate overreaction, Tehran retains flexibility while allowing pressure to build across multiple fronts. This is not a weakness. It is positioning.

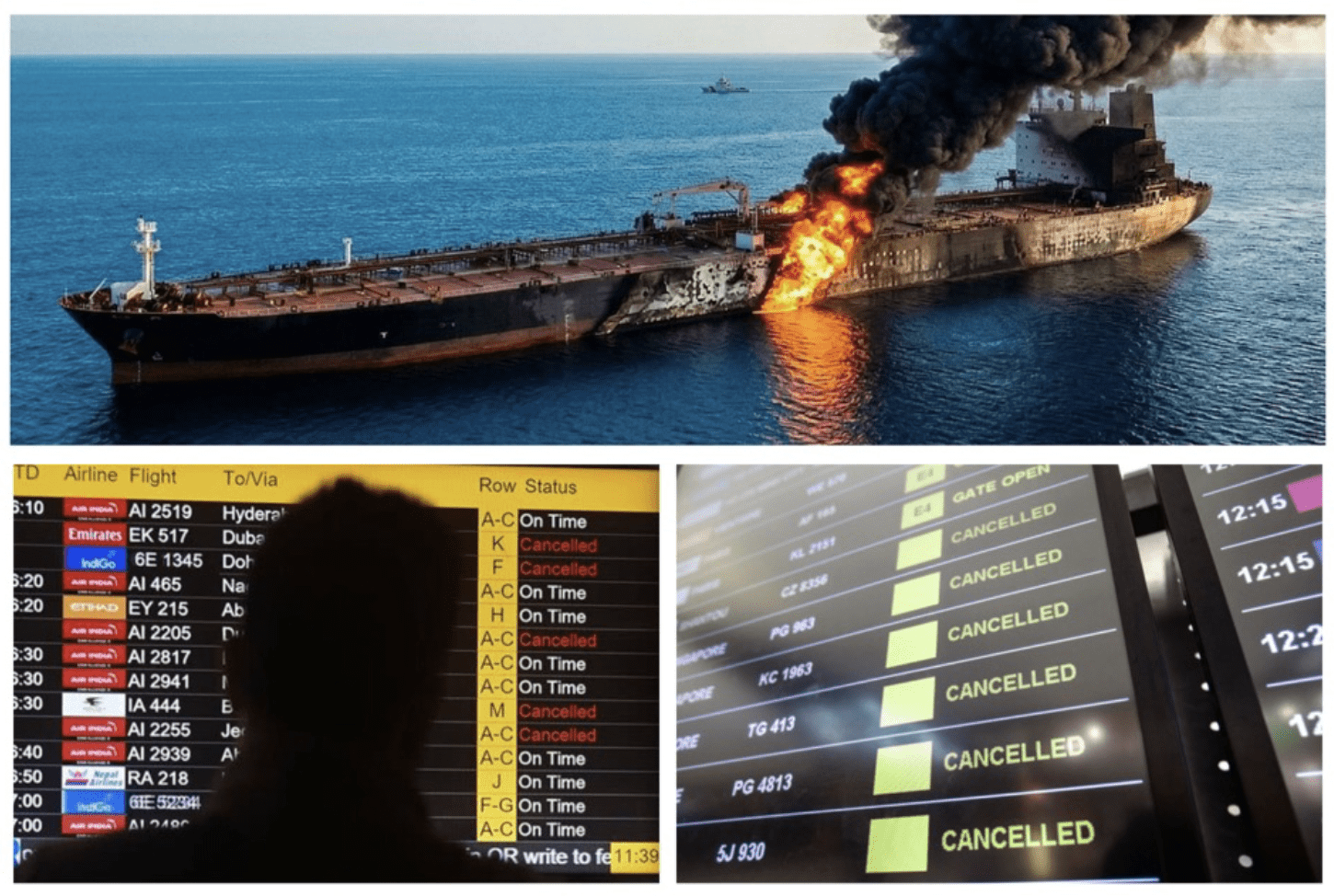

Airspace disruptions across the Middle East have forced airlines to reroute, increasing flight times and operational costs. Key shipping lanes face heightened risk, particularly around the Strait of Hormuz, through which a significant share of global energy supply passes.

Energy markets have responded instantly

Oil prices have surged on the mere perception of disruption. Even limited instability in the Gulf carries disproportionate consequences for global supply chains. For economies already managing inflation and fragile recovery cycles, this is a serious concern.

Tourism is often one of the first sectors to feel the impact

Perception matters as much as reality. Images of conflict, even if geographically contained, travel quickly. Travellers reconsider plans. Insurance costs rise. Airlines adjust capacity. The result is a cooling effect that can extend far beyond the immediate zone of conflict.

For Asia, the implications are indirect but significant

Higher fuel costs place pressure on airlines, which in turn affects fares and route planning. Long-haul travel becomes more expensive. Confidence, always a delicate factor in tourism, becomes harder to sustain.

At the same time, there are potential shifts in travel patterns. Destinations perceived as stable may benefit from diversion, while those seen as exposed could face sudden declines. The balance is fluid and can change quickly.

Financial markets are reflecting this uncertainty.

Energy stocks strengthen while broader indices show volatility.

Investors are recalibrating in real time, weighing risk against opportunity.

What happens next in the Gulf Crisis?

Three paths that could shape energy, markets and global stability

- The first is containment. Diplomatic pressure increases, back-channel negotiations gain traction, and the conflict stabilises without expanding. This is the preferred outcome for global markets and the travel industry.

- The second is controlled escalation. Limited strikes continue, tensions remain high, but both sides avoid actions that would trigger a full-scale regional war. This creates prolonged uncertainty, keeping energy prices elevated and confidence subdued.

- The third is expansion. A miscalculation, a misread signal or an unintended consequence pulls additional actors into the conflict.

At present, the situation sits between the first and second scenarios.

The risk is not only in deliberate action, but in misinterpretation. In a fast-moving environment, signals can be misunderstood. Intent can be misjudged. And events can move beyond the control of those involved.

This is why understanding the adversary matters

Not in a narrow military sense, but in recognising the broader forces at play. Political pressure, economic vulnerability and strategic ambition all shape decision-making. Without that understanding, responses risk being reactive rather than informed.

The Gulf has long been a region where local tensions carry global consequences. What is different now is the degree of interconnectedness. Energy markets, aviation networks and tourism flows are all tightly linked.

A disruption in one area quickly transmits to others

For the travel and tourism sector, the lesson is clear. Agility is essential. Monitoring developments, adjusting capacity and maintaining clear communication with travellers will be critical in the weeks ahead.

For investors and policymakers, the challenge is to navigate uncertainty without overreaction. And for the wider global community, the stakes are high.

This is not simply a regional conflict. It is a test of how power is exercised in a more fragmented, faster-moving world.

The next moves in the Gulf

- From containment to escalation — how this conflict could unfold

- Watch for signals, not statements.

- Diplomacy will continue behind closed doors, even as public rhetoric hardens.

- Oil remains the key indicator.

- Sustained price rises suggest prolonged tension. Sharp spikes may signal escalation.

- Aviation will react quickly.

- Route changes, capacity cuts and fare increases will be early warning signs.

- Markets will stay volatile.

- Short-term swings will reflect uncertainty more than fundamentals.

- The real risk is miscalculation.

In a fast-moving conflict, the greatest danger is not intention, but error.

About the Author

Andrew J Wood is a Bangkok-based travel writer who has lived in Thailand since 1991. With more than four decades in the international hospitality industry, he has held senior leadership roles with several leading hotel groups. A past President of Skål Asia, former National President of Skål Thailand, and a two-time President of Skål International Bangkok, he writes widely on tourism and hospitality trends across Asia and is widely published.

(All images are illustrative representations created by AI for this article and should not be interpreted as factual depictions of real events)