BANGKOK, 13 March 2026: The sudden escalation of military confrontation involving the US, Israel and Iran has sent shockwaves far beyond the Middle East.

For Southeast Asia and Thailand, the conflict may be geographically distant. Yet, its economic consequences could arrive quickly through energy prices, aviation routes, shipping lane disruptions and a dramatic fall in tourism flows.

On Wednesday, a Thai-flagged bulk carrier, Mayuree Naree, was attacked by projectiles in the Strait of Hormuz, causing a fire. News channels reported that the Omani navy rescued 23 Thai crew members. The vessel came under attack when departing from the UAE through the Strait of Hormuz.

As one of the world’s most visited destinations and a major aviation hub linking Europe, the Middle East and Asia, any disruption in global travel patterns or fuel markets is quickly felt across Thailand’s tourism economy. Airlines, airports, hotels and tour operators across the region are already watching developments closely.

Global financial markets reacted swiftly as tensions escalated. Equity markets across the US, Europe and Asia weakened, energy prices climbed sharply, and investors moved toward traditional safe-haven assets such as gold and the US dollar. The initial reaction illustrates how rapidly geopolitical tensions in the Middle East can ripple through global financial systems.

During geopolitical shocks, investors often move toward safe-haven currencies and assets, strengthening the US dollar and the Swiss franc while increasing volatility across emerging market currencies.

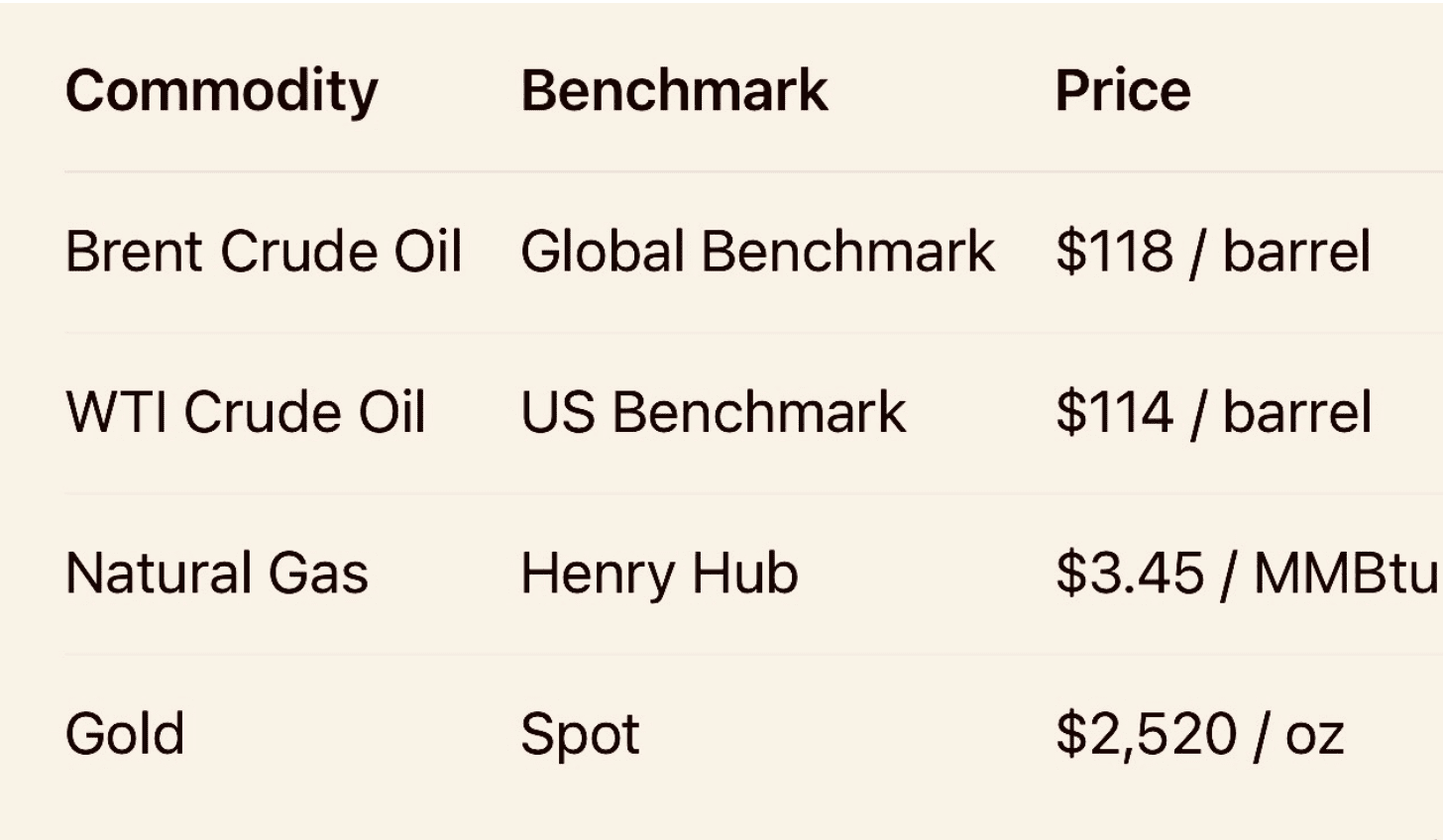

Key energy and commodity prices

Energy markets have reacted particularly quickly to the current crisis. Traders fear potential disruption to Gulf shipping routes and the Strait of Hormuz, through which roughly one-fifth of global oil supply normally passes.

Crude prices spike amid fears of supply disruption in the Gulf

At the height of the market panic, Brent crude surged close to USD120 per barrel before easing again as governments discussed emergency oil reserve releases and diplomatic efforts to contain the crisis. Some analysts warn that if shipping through the Straits of Hormuz were fully disrupted, crude prices could climb toward USD150 per barrel.

There are three possible outcomes from the crisis, each with different implications for Southeast Asia’s tourism-dependent economies.

1. The first possible outcome is what might be called the controlled conflict

Under this scenario, the confrontation remains intense but limited. Iran continues retaliatory missile strikes and cyber activity while the US and Israel avoid expanding the conflict into a broader regional war. Diplomatic channels remain open behind the scenes, and both sides exercise restraint in targeting critical infrastructure or commercial shipping routes.

For Southeast Asia, this would mean turbulence but manageable disruption. Airlines flying between Europe and Asia could temporarily avoid parts of Middle Eastern airspace, adding flight time and increasing fuel costs. Some flights might be diverted northward across Central Asia or take longer southern routes, depending on security conditions.

Even under this limited scenario, Thailand’s tourism sector could feel the strain. If flight interruptions and higher airfares discourage some long-haul travellers, the country could face a tourism revenue hit of roughly THB45 billion over several months.

That figure is substantial. Based on average international visitor spending levels, this would amount to the loss of roughly 900,000 to 1,000,000 international visitors to Thailand. To place this in context, Thailand’s tourism economy is valued at about THB2.7 trillion annually, with approximately THB1.54 trillion generated by international travellers and around THB1.17 trillion from domestic tourism. A THB45 billion decline would therefore represent about 1.7% of the country’s total tourism economy, or just under 3% of international tourism revenue.

2. The second possible outcome could be described as an expanding Middle East war

This scenario concerns global markets far more. If the conflict spreads beyond Iran and Israel and begins drawing in regional allies or proxy forces, the Middle East could quickly become a much wider battlefield.

The Strait of Hormuz remains one of the most critical maritime chokepoints in the world, carrying roughly one-fifth of global oil supply. Any sustained disruption would push energy prices sharply higher and ripple through the global economy.

For Southeast Asia, the consequences would be immediate. Countries across the region depend heavily on imported energy, meaning higher oil prices would translate directly into rising transport costs, airline fuel bills and inflationary pressure.

Shipping routes are also under scrutiny. Some analysts suggest tanker movements could be rerouted further south through the Arabian Sea and into the Red Sea corridor if Gulf shipping becomes too risky. Although longer, this route could provide a temporary alternative. There has also been discussion of naval escort arrangements involving regional partners, including Pakistan, as governments consider how best to protect maritime trade and ensure energy supplies continue to flow.

For export-driven economies such as Thailand, Vietnam and Malaysia, any disruption to global shipping or fuel supply would inevitably ripple through supply chains, manufacturing costs and trade flows.

3. The third possible outcome could become what might be called an Iranian turning point

In this scenario, the conflict triggers deeper political consequences inside Iran itself. The recent strikes could weaken the country’s leadership structure or provoke domestic instability, potentially opening a period of internal political turbulence.

Alternatively, the Iranian government might emerge hardened and more determined, strengthening its strategic posture and accelerating its military ambitions. Either direction could reshape the geopolitical balance of the Middle East and introduce longer-term volatility into global energy markets.

Thailand tourism exposure by source markets

Thailand’s tourism exposure also varies widely by source markets. Short-haul regional visitors represent a large share of arrivals, but long-haul travellers from Europe, Australia and the Middle East typically stay longer and spend more per trip. These travellers are also the most likely to be affected by aviation disruptions or extended flight routes due to Middle Eastern airspace tensions.

Thailand Tourism Exposure by Source Markets: China remains Thailand’s largest market, though Europe and India continue to grow.

Long-haul markets are particularly important for Thailand because these visitors typically stay longer and generate higher per-trip spending across hotels, dining, shopping and excursions.

For Thailand, the implications are clear. Tourism, aviation and trade are deeply connected to global stability. Higher fuel prices, longer flight routes and cautious travellers could all weigh on visitor numbers and industry confidence.

Yet Southeast Asia has demonstrated resilience during previous global shocks. Diversified tourism markets, strong regional connectivity and adaptable businesses have often helped the region absorb external crises and recover quickly.

About the author

Andrew J Wood is a British travel writer and hotel industry commentator based in Bangkok. A former general manager of several leading hotels in Thailand, he has spent more than three decades working in the Asian hospitality industry. He is a former Director of Skal International Bangkok and a long-standing observer of the tourism industry who writes regularly on travel, tourism development, and regional economic trends across Southeast Asia.